Hello! Welcome to Embedic!

In December 2020, many MCU manufacturers announced price increases. ST officially issued a price increase notice a few days ago. Starting January 1, 2021, the price of all products will increase; before ST announced the price increase, Shengqun (Hetai), Lingtong, Songhan, Hongkang, Nuvoton The five major Taiwanese MCU manufacturers also publicly stated that due to rising costs, they have simultaneously increased their product prices. Some items have been adjusted by more than 10%, and product delivery dates have even been extended to 10 months. In addition, Japanese MCU manufacturer Renesas Electronics also issued a price increase notice not long ago, and the delivery period has been extended to more than 4 months.

There may be several reasons for the MCU out-of-stock price increase:

1, the time period from wafer to chip shipment is about half a year. It actually takes a long time for a chip to design, manufacture, package, test, and then ship. Even if the time for design and trial production is not counted, for a mature chip using mature technology, it usually takes about half a year from the beginning of wafer manufacturing, to packaging and testing, and then to shipment. Therefore, the original chip factory is scheduled according to the order, and the production capacity is pre-arranged. After all, the stocking of wafers requires real money. If the stock is too much and not sold, the original factory will be very harmful.

2. the chip factory has reduced wafer stocking. At the beginning of this year, the new crown epidemic broke out suddenly, and all walks of life were affected for a while. Many factories shut down, trade was also blocked, many companies laid off employees, reduced expenditures and reduced expenditures. In the first half of the year, everyone expected the future. Generally not optimistic. After seeing this situation, the original factory chose to reduce wafer stocking when planning in the first half of the year. It is said that some original factories reduced stocking by more than 1/3.

3.Huawei was suppressed by the US government, which caused Huawei to increase orders in its foundries. As a result, China’s major packagers in June, July, and August were basically all orders from Huawei, and other Chinese semiconductor manufacturers. It is basically difficult to get production capacity. Can only go back.

4.due to the Sino-US trade conflict, Huawei is greatly affected by the United States. Many of Huawei's chip products cannot be produced due to sanctions, such as Huawei's Kirin processor chips, Honghu chips for smart TVs, security chips, and server storage. Chips, Baron series chips, etc.

Especially for the IPCSoC chips used by security, Huawei previously accounted for more than 70% of this market, and now it cannot be produced at once, but the market demand has not diminished. This requires products from other companies to fill this market. . Therefore, other Chinese companies have placed orders to foundries, but many of these chips are new designs of newly entered companies. Trial production of wafers needs to occupy the production line of the foundry, and the yield rate of new chips will increase. It often takes time. Now these new products will greatly reduce the production efficiency of wafer foundries and packaging plants, and shipments will be slow.

5. China's electronics industry began to recover as a whole in the second half of the year, especially in overseas markets. The backlog of overseas orders in the first half of the year broke out all at once, but many factories basically did not stock up in the first half of the year. Suddenly, orders surged, and the previous production capacity of the original chip factory could not meet the demand.

6.during the off-season, foundries will generally give their production lines to low-profit products such as MOSFETs, but once the peak season comes, they will generally give way to high-profit ICs. The second half of the year is peak season in China and abroad. Therefore, many MOSFETs and low-profit MCUs are more difficult to obtain production capacity.

7. the demand for China’s new infrastructure and the Xinchuang industry has soared. The original factories that had reduced their stocking plans began to increase stocking and began to place large orders for fabs. In this way, under the squeeze of large customers, small orders were squeezed. The demand scheduling of customers and small customers is often delayed.

It is precisely because of the superposition of these multiple factors that the semiconductor market has begun to have tight production capacity and supply shortages. Coupled with the impact of the price increase of wafer foundries and packaging plants, chip makers have also had to increase chip prices.

On September 14, NVIDIA and SoftBank announced a definitive agreement under which NVIDIA will acquire British chip design from SoftBank and its Vision Fund for US$40 billion Subsidiary Arm.

According to the agreement, Nvidia will pay SoftBank Group US$12 billion in cash and US$21.5 billion worth of Nvidia shares, including the US$2 billion immediately paid when the contract is signed.

The 2 parties said in a joint statement that if Arm’s future performance reaches a specific target, SoftBank may also receive an additional $5 billion in cash or stock. After the acquisition, NVIDIA will also issue $1.5 billion in equity to Arm employees.

If Nvidia succeeds in acquiring Arm, it will be one of the largest M&A transactions this year, and it may also be the largest semiconductor transaction in history.

The acquisition of Arm will change NVIDIA’s current over-reliance on GPU products. Through this acquisition, NVIDIA will obtain more mobile CPU/GPUIP, which will greatly enrich its product line and allow NVIDIA to enter the mobile processor field. At the same time, it is expected to extend its advantages on the graphics card end to the mobile end.

However, because NVIDIA itself has a competitive relationship with some of Arm’s existing customers, this also makes the outside world worry that the acquisition of Arm by NVIDIA will affect the neutrality of Arm, which causes Arm’s customers to turn to its competitor RISC-V.

In October, Japanese MCU manufacturer Renesas Electronics announced the launch of technology IP cooperation with AndesTechnology, a supplier of RISC-V architecture embedded CPU cores and related SoC development environments. Renesas chose AndesCore 32-bit RISC-VCPU core IP to apply to its new dedicated standard products, and will begin to provide customers with samples in the second half of 2021.

In December, China Micro Semiconductor announced the official release of the first 32-bit microcontroller with integrated RISC-V core-ANT32RV56xx. This series of chips is equipped with NucleiSystemTechnology (NucleiSystemTechnology) N100 series of ultra-low-power RISC-V processor cores, integrates analog peripherals and simplifies design, and easily responds to consumer electronics' requirements for high computing power and low power consumption.

Also in December, Zhongke Lanxun also launched an independent RISC-V core 32-bit MCU chip ------ Lanxun Jiaolong AB32VG1. This MCU provides a 125MHz operation frequency (up to 192MHz). ), on-chip integrated RAM192Kbyte, Flash1Mbyte, ADC, DAC, PWM, USB, SD, UART, I2C and other resources. Lanxun Jiaolong AB32VG1 evaluation board will be launched simultaneously, and a complete SDK will be provided. Developers can use the free RT-ThreadStudio integrated development environment to quickly get started, and easily complete a series of development such as code writing, compilation, debugging, and programming. Process.

Before them, Zhaoyi Innovation and launched RISC-V core MCU products in 2019, and Pingtou launched and open sourced its RISC-V chip design platform.

It can be seen that more and more players have gradually joined the RISC-V camp, and the ecology of RISC-V has also begun to become enriched. In the future, RISC-V will not only gain attention, but also achieve greater development. .

On December 4, there were media reports that the semiconductor industry's production capacity problem was transmitted to the automotive industry. Due to the lack of automotive chips, the two modules, ESP (Electronic Stability Program System) and ECU (Electronic Control Unit), SAIC Volkswagen and FAW Volkswagen will face production suspension risk.

Although FAW-Volkswagen responded on December 5, saying that the production of new cars was indeed affected to a certain extent, but it did not completely stop production as rumors outside. From the response, it can be seen that the shortage of automotive-grade chips does exist.

Car-level chips can be divided into MCU, memory chips, power devices (IGBT and MOSFET), ISP, power management chips, radio frequency devices, sensors (CIS, acceleration sensors, etc.), GPU/ASIC/FPGA/AI chips, etc.

In 2020, the global automotive-grade chip market is expected to be 300 billion yuan, accounting for about 10% of the global semiconductor market. According to estimates, in the future, the value of car-grade chip bicycles will increase from 2,800 to 12,000 .

For example, in terms of MCUs, traditional cars use more than 70 MCU chips per car on average, and each smart car is expected to use more than 300 MCU chips. The demand for automotive-grade MCUs will increase significantly.

In addition, global automotive-grade chip companies mainly include NXP, Infineon, Renesas, Texas Instruments STMicroelectronics, etc. The top 8 companies have a market share of 63%. At present, the automotive-grade chip market is mainly occupied by foreign manufacturers, and there is huge room for substitution in China.

In August 2020, NXP (NXP) released the eIQ machine learning (ML) software to support Glow Neural Network (NN) compiler, which is aimed at NXP's i.MXRT crossover MCU, bringing the industry's first implementation to Lower memory footprint provides higher performance neural network compiler applications. The Glow compiler was developed by Facebook and can integrate target-specific optimizations. NXP uses this ability to use the neural network operator library suitable for ArmCortex-M core and CadenceTensilicaHiFi4DSP to maximize i.MXRT685 and i.MXRT1050 and The reasoning performance of RT1060. In addition, this feature has been integrated into NXP's eIQ machine learning software development environment and is provided free of charge in NXP's MCUXpressoSDK.

ST launched the STM32Cube.AI toolkit in 2019, which can interoperate with popular deep learning libraries, convert and apply any artificial neural network to STM32 microcontrollers (MCUs). The Cube.AI tool is an AI expansion package of CubeMX, which can be downloaded in CubeMX or separately.

The neural network model frameworks supported by STM32Cube.AI include Lasagne, Keras, Caffe, ConvNetJs, TensorflowLite, and frameworks that can be exported to ONNX standards (PyTorch™, Microsoft® Cognitive Toolkit, MATLAB® and more).

In December, the Chinese IoT operating system RT-Thread launched the end-side AI development kit AIKit for developers at its developer conference to help solve the problem of fragmentation of end-side deployment of AI. The tool adopts an open architecture. The tool-side platform construction smoothly integrates the upstream model to the specific hardware platform engine and runtime library into an RT-Thread integration framework project. Therefore, RT-Thread's AIkit can be deployed with one click without knowing the processor optimization method, and developers can devote most of their energy to product development.

According to Jin Guangyi, marketing director of Beijing Zhaoyi Innovation and Technology Company, from 2013 to 2019, GD32 shipments continued to rise, with a compound annual growth rate of 201%, reflecting the continued development momentum of products and continuing to be the development of intelligent hardware in the Internet of Things field. Boost. As of October 2020, MCU shipments have exceeded 150 million. The company has shipped 500 million MCU products and the number of customers exceeds 20,000. MCU has become the second-highest product of Zhaoyi Innovation.

Zhang Jianwen of Huada Semiconductor Co., Ltd. revealed in public that Huada also provided the MCU required for the on-board OBU equipment in China's ETC system, which accounts for 50% of the demand. From the outbreak of the epidemic to November in 2020, BGI provided at least 25 million thermometer chips for the market.

In addition to these two, MCU manufacturers such as Smart Microelectronics, National Technology, Jihai Semiconductor, Hangshun, and China Micro Semiconductor have also increased their shipments this year.

In July, Arm China (Arm China) released the R&D process, characteristics and implementation status of the first Chinese-oriented processor-the "Star" processor (STAR-MC1). At present, the processor has officially entered the commercial stage.

STAR-MC1, as the first product in the "Xingchen" series, supports all the features of the existing Armv8-M architecture and the latest command extensions. According to Liu Shu, vice president of R&D of Amou China Products, this processor is a very tightly coupled high-efficiency microprocessor with a performance of 1.5DMIPS/MHz-4.02Coremark/MHz, and inherits the structure of Armv7 and Armv8. DSP instructions and floating point calculation unit. Compared with the previous generation of Arm processors, under the same main frequency, these new structural system upgrades can increase the performance of STAR-MC1 by 20%.

In March, NXP Semiconductors announced the launch of the i.MXRT600 crossover microcontroller (MCU), which is an ideal solution for ultra-low-power, secure edge applications such as audio, voice, and machine learning. The i.MXRT600 crossover MCU has outstanding features in terms of power consumption, performance and memory. mainly include:

Arm®Cortex®-M33 core with a frequency of up to 300MHz.

Optional Cadence®Tensilica®HiFi4 audio and voice digital signal processor (DSP). The operating frequency is up to 600MHz and supports four groups of 32x32MAC.

Up to 4.5MB of on-chip SRAM supports "zero-wait" access of key instructions and data.

The 28nm FD-SIO (depletion-mode silicon-on-insulator) process provides lower operating current and leakage current.

Built-in NXP's superior embedded security technology-EdgeLock400A.

The Glow neural network compiler can be used to optimize machine learning performance.

ST also launched the STM32MP1 cross-border, which is the first general-purpose STM32MPU, dual-core Cortex-A+Cortex-M multi-core architecture, stronger computing power; flexible architecture can meet high performance, hard real-time, low power consumption and safety At the same time, it also inherits the STM32 ecosystem, not only has a variety of hardware development boards, three types of software development kits, etc., but also can port the previous M4-based control to MP1, thereby accelerating the progress of product development.

As a complement to the STM32RF connectivity product portfolio, the STM32WL system-on-chip integrates a general-purpose microcontroller and sub-GHz wireless control unit on the same chip. It is the world's first wireless microcontroller that integrates a LoRa transceiver on an SoC chip. Previously, the LoRa wireless solutions on the market were either discrete microcontrollers and transceivers, or the two components used the same package but used different die, that is, system-in-package. STM32WL empowers IoT applications by achieving simpler, more flexible, higher integration and more energy-efficient designs.

In October of this year, the STM32WB wireless MCU product line added a new product. The low-cost version of STM32WB55, STM32WB35/30, will push the price/performance ratio to the extreme.

In terms of cost, compared to STM32WB55/50, STM32WB35 has a lower cost. STM32WB30 is the lowest cost ST Bluetooth+802.15.4 solution.

In terms of peripherals, compared with STM32WB55, STM32WB35 has no LCD;

In terms of radio frequency, STM32WB55 supports dynamic multi-protocol, and STM32WB35/50/30 only supports a certain protocol;

In terms of packaging, STM32WB55 has the most package types. STM32WB35/50/30 have only QFN48 and are compatible with STM32WB55QFN48pin2pin.

In July of this year, NXP announced that MCUXpresso supports its Wi-Fi®/Bluetooth® combination solution and i.MXRTMCU crossover processor, which greatly simplifies product development. With this new integration capability, NXP has expanded the connectivity capabilities of EdgeVerse™ edge computing and security platforms.

By pre-integrating driver support in MCUXpressoSDK, NXP provides developers with a flexible and extensible platform to help accelerate compliance, significantly reduce time to market, and simplify the deployment of Wi-Fi or Wi-Fi/Bluetooth combinations. These new platforms make it possible for MCU, Wi-Fi or Wi-Fi/Bluetooth combination devices to work together to help developers flexibly meet the performance and power consumption requirements of IoT, industrial, automotive, and communication infrastructure applications.

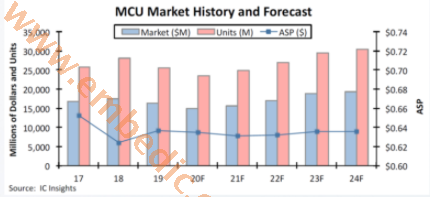

According to a report released by ICInsights in August this year, in 2019, the global MCU market is about 16 billion U.S. dollars. Due to the impact of the new crown epidemic, it is expected to fall to 14.9 billion U.S. dollars this year, a drop of about 6% . But in China, the MCU market is actually growing, and Chinese MCU companies have basically achieved positive growth in their shipments in the first half of the year.

In fact, the market size of China's MCU is not small. According to statistics, China's market size in 2019 is 36.6 billion yuan, and it is expected to reach 48.4 billion yuan by 2024, but the market share of China's MCU products is not high. Zhong Xinli of National Technology said that in the world, 8-bit MCUs and 32-bit MCUs each account for half, but China is still dominated by 8-bit MCUs. 32-bit MCUs are still in the catching-up stage, and the growth trend is relatively obvious.

Liu Tao of Jihai Semiconductor also holds the same view, but he gave another figure, that is, the market share of China's MCU products is currently not high. In the Chinese market, China's MCU market share is less than 10%. Less than 5% of China-like MCUs, and even lower proportions of Chinese MCUs in the automotive category, he estimated less than 1%.

in recent years, the shipment volume of Chinese MCU companies has been steadily increasing. the reason for the positive growth in the shipment volume of Chinese MCU companies is mainly driven by the following 5 factors. The market has brought new growth momentum.

1. the development of 5G and the Internet of Things has led to the rise of smart homes;

2. the upgrading of home appliance MCUs, which will increase the size of the MCU market;

3.the implementation of the new national standard for electric bicycles, coupled with the impact of the epidemic, the electric bicycle market ushered in new growth opportunities. For example, in Europe, due to government subsidies and the inconvenience of public transportation during the epidemic, many people choose electric bicycles to travel, which stimulated the export of Chinese electric bicycles;

4.MCU is increasingly used in lithium battery management chip applications;

5.the Sino-US trade war has made more and more Chinese system manufacturers more inclined to use Chinese chip products.

Manufacturer: Texas Instruments

IC DSP FIXED-POINT 196NFBGA

Product Categories: DSP

Lifecycle:

RoHS:

Manufacturer: Microchip

IC MCU 8BIT 28KB FLASH 44TQFP

Product Categories: 8bit MCU

Lifecycle:

RoHS:

Manufacturer: Microchip

IC MCU 8BIT 32KB FLASH 40DIP

Product Categories: 8bit MCU

Lifecycle:

RoHS:

Manufacturer: ON Semiconductor

IC AUDIO PROCESSOR AD/DA 57CABGA

Product Categories: DSP

Lifecycle:

RoHS:

Looking forward to your comment

Comment

1

2

3

4

5

6

Popular Searches

Popular Searches8 Bit MCU, Flash, PIC16 Family PIC16F7XX Series Microcontrollers, 20 MHz, 7 KB, 192 Byte, 44 Pi...

EEPROM 2K 256 X 8 2.5V SERIAL EE IND

System-On-Modules - SOM RCM2200

32-bit Arm Cortex-A53 vision processor with ISP, powerful 3D GPU, dual APEX-2 vision accelerat...

IC MCU 8BIT 60KB FLASH 44QFP

DSP 20MHZ 44QFP

Product updates, events, and resources in your inbox

Smart System

Traffic Management

Security

Consumer Electronics

Wireless Technology

Robot

Internet of Things

Industrial Control